Markets

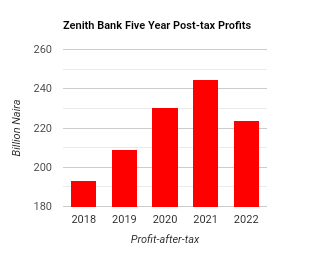

High bad loans provision lowers Zenith Bank’s profit by 8.44% to N244.56bn

As inflation accelerated and the economy of the country struggled, Zenith Bank had to make more provisions for bad loans and spend more on operations in 2022, which slowed the growth rate of its profit, its recent financial statement for 2022 has shown.

The bank’s profit after tax lowered by 8.44 per cent to N223.91 billion in 2022 from the N244.56bn it made in the prior year.

This was the first time Zenith Bank’s post-tax profit will decline since 2013 when it dropped by 5.32 per cent. 230.

Nigerian most capitalised banks reported a drop in post-tax profit in 2022 as a result of high provisions for bad loans, which soared by 106 per cent to N123.25 billion compared to N59.53 billion in 2021, and operating costs, which increased 17.32 per cent to N339.69 billion in 2022, as a result of higher staff costs and a 69.57 per cent increase in income tax costs to N60.74 billion from N35.82 billion in 2021.

Understandably, its cost-to-income ratio went up by seven per cent to 54.4 per cent from 50.8 per cent in 2021.

The lender said the rise in impairments was partly due to Ghana’s sovereign debt restructuring programme. a

Despite this, profit before tax increased slightly by 1.53 per cent, from N280.37 billion to N284.65 billion, due to growth in all income lines.

It spent 63 per cent more on interest and related revenue in 2022 than it did in 2021, spending N173.54 billion instead of N106.79 billion.

The lower-than-expected bottom line of Zenith Bank is a contrast to its impressive topline, with double-digit growth of 23.51 per cent in gross earnings to 2021 to N945.55 billion in 2022, from N765.55 billion in the preceding year.

The growth in revenue was driven by an increase of 26.33 per cent year-over-year in interest and similar income from N427.59 billion to N540.16 billion as investment securities in treasury bills, bonds, and other securities increased.

The global increase in interest rates moved the cost of funding up from 1.5 per cent in 2021 to 1.9 per cent in 2022.

The bank’s Net Interest Margin also benefitted from the persistently high yield environment as it increased to 7.2 per cent from 6.7 per cent as a result of an efficient repricing of interest-bearing assets.

It also grew its gross loans by 17.76 per cent to N4.12 trillion, from N3.50 trillion in 2021 as the country’s economy continued on a recovery path.

Zenith Bank’s customer deposits increased by 38.68 per cent, growing from N6.47 trillion recorded in the previous year to N8.98 trillion in 2022.

The loan-to-deposit ratio of the bank arm of the group dipped by 18 per cent to 51.6 per cent during the period under review from 62.6 per cent in 2021, with the group’s loan-to-deposit ratio dropping by 15 per cent to 45.9 per cent.

This is below the regulatory benchmark loan-to-deposit of 65 per cent.

The return on average equity also worsened by 18 per cent to 16.8 per cent from 20.4 per cent in 2021.

Similarly, its Capital Adequacy Ratio declined by six per cent to 19.8 per cent against 21 per cent in the prior period, while was still way above the 15 per cent the Central Bank of Nigeria requires.

Expectedly, the non-performing loan was up by three per cent to 4.3 per cent in 2022, compared to 4.2 per cent, still below the regulatory five per cent benchmark.

Meanwhile, the liquidity ratio of the group improved by five per cent to 75 per cent instead of the 71.6 per cent it had in the previous year. The CBN pegged the liquidity ratio at 30 per cent.

For the bank, the liquidity ratio bettered by eight per cent to 67 per cent, compared to 61.9 per cent in 2021.

Despite the drop in its post-tax profit, the bank has proposed to pay a final dividend of N2.90 per share, bringing the total dividend for 2022 to N3.20 per share.

Like many of the tier-one lenders in the country, Zenith Bank has got the nod of the CBN to operate a non-operating financial holding company structure, which would allow it own subsidiaries in other sub-sectors of the financial market.

It has resolved to broaden its horizons in 2023 while simultaneously restructuring into a holding company structure, increasing in all of its chosen domestic and foreign markets, and adding new verticals to its companies.

US authorities slam Air Peace boss, Onyema, with fresh fraud charges

Report: NUPRC has not approved $1.3bn Shell Renaissance deal

There’s a plan to derail Tinubu’s petroleum industry revolution

NNPCL’s acquisition of OVH: Reps member, Miriam Onuoha, slams Atiku, says oil and gas sector should not be politicised

Fidelity Bank affirms commitment to data protection, strong corporate governance

NGX rates Fidelity Bank highest on corporate governance

Like Saudi Aramco, NNPC Ltd under Kyari is creating value for Nigerians

NNPCL FY’23: Kyari stands tall in spite of disruptors’ intrigues

Arewa groups accuse Ugochinyere of plot to blackmail Speaker Abass, deputy, call for probe

CNPP and its failed evil campaign against NNPCL, Kyari

Arewa youths slam Dangote, say ‘you can’t dictate fuel price’

Warn Agbese over false allegations against NNPCL, NMDPRA, group tells reps speaker

1XCUP 2024: 20 teams to battle for N20m as competition kicks off August 5

Paris 2024 Olympic table tennis draw announced